Decoding the New Market DNA – 2026 Generational Homebuying Trends

How are different generations shaping the 2026 housing market?

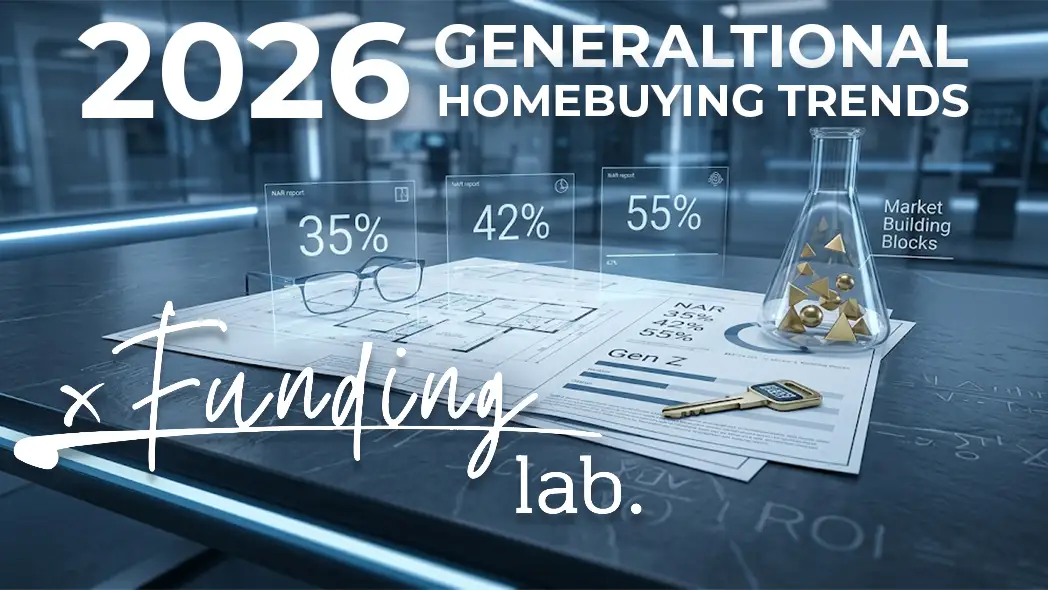

Recent data highlights a major shift in homeownership demographics across the United States. Specifically, the 2026 Generational Homebuying Trends report indicates that Baby Boomers control 42% of all purchases. Simultaneously, Gen Z women represent 35% of single female buyers, while Older Millennials maintain the highest household incomes.

The New Faces of Homeownership

The 2026 real estate market is no longer a monolith. Instead, it is a complex ecosystem of distinct age groups with varying financial strengths. According to the latest National Association of Realtors (NAR) report, we are seeing a fascinating “generational handoff.”

While Baby Boomers represent a staggering 55% of home sellers, they are also re-entering the market as powerful buyers. Furthermore, a new wave of younger investors and homeowners is emerging. Specifically, Gen Z is making its presence felt among single female buyers. Consequently, these 2026 Generational Homebuying Trends dictate everything from inventory availability to mortgage product demand. At The Funding Lab, we believe understanding these demographics is the first step toward a successful transaction. Whether you are selling a family estate or buying your first condo, these figures represent the current pulse of the American dream.

The Lab Data Breakdown: 2026 Generational Market Snapshot

| Buyer Segment | Market Share | Defining Characteristic | Key Market Impact |

| Gen Z | 35% (Single Females) | Rapidly rising first-time buyers | Increased demand for entry-level homes |

| Older Millennials | Varies | Highest Median Household Income | Dominance in the “move-up” luxury market |

| Baby Boomers | 42% (All Buyers) | Significant cash reserves/equity | Competitive advantage in bidding wars |

| Baby Boomers | 55% (All Sellers) | Primary source of market inventory | Dictates overall housing supply levels |

Solution Sam’s Perspective

Look closely at the data “compounds” in our latest report. The 2026 Generational Homebuying Trends reveal a market where experience meets high-earning potential. Specifically, Older Millennials are currently the “power hitters” regarding income. Therefore, they often compete for the same high-end suburban inventory that Boomers are vacating.

Think of the market like a pressurized filtration system. Boomers are the primary “source,” providing over half of the available homes for sale. However, they aren’t just leaving the market; they are cycling back in. This creates a “loop” that keeps prices stable but inventory tight.

Solution Sam Pro-Tip

In my experience, many buyers look only at the interest rate. However, the real “gotcha” in 2026 is the competition profile. If you are a younger buyer, you are often competing against Boomers who have 30 years of equity. To win, your “Formula for Success” must include a fully underwritten pre-approval. This proves your financial stability is just as reactive as a cash offer.

We see this playing out across the country. Whether in the Midwest or the Sunbelt, the generational overlap is the defining story of the year.

Why do Older Millennials have a buying advantage in 2026?

Older Millennials hold an advantage because they currently possess the highest median household income of all buyer groups. This financial strength allows them to navigate higher interest rates more effectively. Additionally, they often have established credit profiles, making them ideal candidates for both traditional and specialized mortgage products.

What does this all mean?

Ultimately, the 2026 Generational Homebuying Trends reveal a market defined by diversity and resilience. While Baby Boomers provide the necessary inventory and maintain a strong buying presence, younger generations are rewriting the rules of entry. Specifically, the rise of Gen Z female buyers and the high earning power of Millennials are creating new opportunities for growth.

At The Funding Lab, we understand that these shifting demographics require more than a one-size-fits-all loan. Consequently, we focus on the precise math and specialized products needed to help every generation secure their piece of the American dream. Whether you are ready to downsize or move up, the right formula makes all the difference.

Reach out and let us start building a formula just for you.

Terms You Should Know

- Median Household Income: The midpoint of all family incomes in a specific demographic, used to gauge overall purchasing power.

- Inventory Turnover: The rate at which available homes are sold and replaced by new listings in the housing market.

- Underwritten Pre-Approval: A rigorous lender review process that verifies income, assets, and credit before a buyer finds a property.

Frequently Asked Questions (FAQ)

Yes. Specifically, the data shows Gen Z women are entering the market at a higher rate than previous generations at the same age.

Many Boomers are “right-sizing.” Consequently, they sell large family homes and immediately purchase smaller, more accessible properties.

Higher income generally allows for a more flexible Debt-to-Income (DTI) ratio. However, credit health remains a critical component of the final equation.