What is a P&L Loan? 2026 Guide for Self-Employed Borrowers

What is a P&L Loan and how does it work?

A P&L Loan is a Non-QM mortgage designed for self-employed borrowers that uses a business Profit and Loss statement to calculate income instead of IRS tax returns. This specialized program allows entrepreneurs to qualify for financing based on their actual business profitability and current cash flow performance.

Your Business Success is Your Credit

Specifically, tax season is a double-edged sword for the modern entrepreneur. You work hard to maximize legal deductions. Consequently, your taxable income often appears too low for traditional bank financing. Therefore, you are trapped between saving on taxes and qualifying for a new home. At The Funding Lab, we believe your business success should be rewarded, not punished. Specifically, a P&L Loan looks at your current trajectory. It values your real-world earnings over historical tax filings. This guide explains how to leverage your business data to secure your next property.

The Lab Data Breakdown: Underwriting Comparison

| Feature | Standard Full-Doc Loan | The Funding Lab P&L Loan |

| Loan Classification | Conforming / Qualified Mortgage | Non-QM (Non-Qualified) |

| Primary Income Doc | 2 Years of IRS Tax Returns | 12-Month P&L Statement |

| Impact of Deductions | Reduces Borrowing Power | Minimal (Real expenses only) |

| Asset Reserves | Standard (2-6 Months) | Higher (6-12 Months) |

| Approval Speed | Up to 90 Days (Tax verification) | 30-45 Days (Asset-based focus) |

Solution Sam’s Perspective

In my experience, entrepreneurs fail at mortgages because they focus on math rather than behavior. Specifically, the emergency fund prerequisite is non-negotiable for a P&L loan. Lenders give you a “pass” on tax returns. Consequently, they want to see deep liquidity as a safety net.

We often talk about the minimum payment rule. Lenders analyze your business debt service just as closely as your personal debt. Therefore, keeping your business overhead lean in the six months leading up to an application is vital. Remember The Roll-over Effect: if you pay off a small business equipment lease early, you instantly boost your “paper income” on that P&L.

Solution Sam Pro-Tip

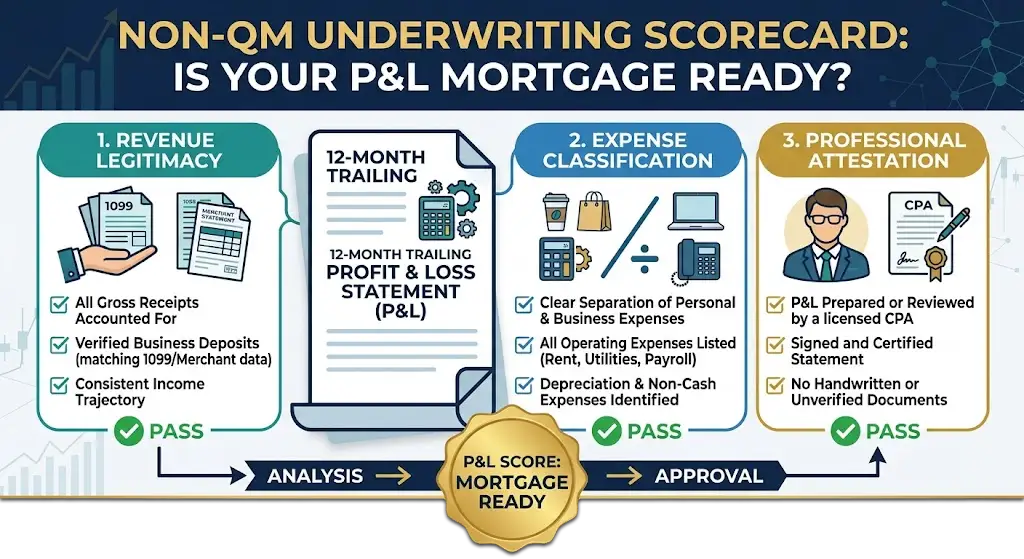

Never present a handwritten P&L. Even if you are a “solopreneur,” have your P&L prepared or at least signed by a CPA. It adds instant institutional credibility to your file and signals that your business is a professional entity, not just a hobby.

Terms to Know

- Non-QM (Non-Qualified Mortgage): A loan that does not follow standard government-backed rules, allowing for flexible income verification.

- Debt-to-Income (DTI) Ratio: The percentage of your monthly gross income that goes toward paying debts.

- Soft Inquiry: A personal credit check that does not affect your score.

Will a P&L Loan have a higher interest rate?

Yes, P&L Loans typically carry a slightly higher interest rate than traditional conforming mortgages. Lenders perceive higher risk because they do not verify income via the IRS. However, the trade-off allows you to keep your tax deductions while still moving into your new property on your terms.

Do I need to be self-employed for a specific amount of time?

Most P&L programs require you to be self-employed for at least two full years. Lenders look for stability and a consistent track record of revenue. Specifically, they want to see that your business is a reliable source of income for the foreseeable future. There may be exceptions available depending on your unique situation. Ask a mortgage professional to see if you may still qualify with less than two years in business.

What is the difference between a P&L Loan and a Bank Statement Loan?

A P&L Loan uses a summary statement, while a Bank Statement Loan requires actual deposit records. Specifically, the P&L method is often better for businesses with higher overhead. In contrast, Bank Statement loans use a fixed “expense factor” that may not fit every business model.

Can I use a P&L Loan for an investment property?

Absolutely, P&L Loans are excellent tools for real estate investors and “house hackers.” Since investors often show high depreciation on tax returns, the P&L method reveals the true profitability of their portfolio. Consequently, you can scale your investment business faster using business cash flow records.

Can I get a P&L Loan with a low credit score?

While P&L loans are flexible on income, they usually require a higher credit score (typically 680+) to offset the risk. Because the lender is not seeing your tax returns, they rely heavily on your credit history to prove financial responsibility. Therefore, improving your score before applying is a smart move. Again, there may be exceptions available. Be sure to speak with a loan professional to see if you qualify.

How do I prepare my business for a P&L Loan?

Start by ensuring your bookkeeping is updated and professionally reviewed. Specifically, you should separate personal and business expenses completely. Additionally, minimize large business purchases right before applying. This keeps your debt-to-income ratio healthy.

Step-By-Step Process Map

Preparing for P&L Loan Approval

- Audit Your Books

Reconcile every transaction for the last 12 months.

- Download our CPA-Ready P&L Template

Use this to format your data for our underwriters.

- CPA Certification

Have an independent professional sign off on your Profit and Loss statement.

- Liquidity Prep

Ensure your emergency fund is in a liquid account.

- Submit to The Funding Lab

We match your data to the best program for your needs.

Frequently Asked Questions (FAQ)

Yes, The Funding Lab provides these loans across the United States. However, borrowers in states like California or Florida may see variations in loan limits or regional high-balance programs.

Lenders generally require proof that your business is active and legal. Specifically, they may ask for a business license, Articles of Incorporation, or a letter from your CPA confirming you have been in business for two years.

Yes, The Funding Lab offers these for both residential and commercial real estate. Because commercial loans are already based on business income, a P&L statement is a standard part of the process.

Most negative items stay for seven years. Specifically, this includes late payments and foreclosures. However, Chapter 7 bankruptcies can remain for ten years.

Learn More

To master your finances, you should also understand Debt-to-Income Ratios, Amortization Schedules, and Non-QM Lending. These factors impact your long-term wealth as much as your initial loan type.

Have additional questions about P&L Loans or other Non-QM Loan programs? Reach out! Through our strategic partnerships we can connect you with the perfect credit team!

Download the CPA-Ready P&L Template

Preparing your business records for a mortgage doesn’t have to be a headache. To help you move faster, The Funding Lab has developed a 12-Month Trailing Profit & Loss Template specifically aligned with Non-QM underwriting standards.

How it works:

- Plug-and-Play: Simply enter your monthly revenue and expenses into the data entry tab.

- Automatic Logic: The template automatically calculates your totals and prepares a clean, professional summary page.

- Professional Alignment: Every category is designed to match standard accounting practices, making it easy for your CPA to review and sign.

- Universal Compatibility: You can download the file to use in Microsoft Excel or easily upload it to Google Sheets to manage your data in the cloud.

Before you meet with your accountant, use this tool to see exactly where your “Mortgage-Ready” income stands.